Works on: Windows 10 | Windows 8.1 | Windows 8 | Windows 7 | Windows XP | Windows 2000 | Windows 2003 | Windows 2008 | Windows ME | Windows Vista | Windows 2012 SHA1 Hash: 0e282bbec011940e75cf19091cf71f830cf9f281 Size: 601.61 KB File Format: zip

Rating: 2.304347826

out of 5

based on 23 user ratings

Publisher Website: External Link Downloads: 265 License: Demo / Trial Version

Portfolio Optimization is a demo software by Business Spreadsheets and works on Windows 10, Windows 8.1, Windows 8, Windows 7, Windows XP, Windows 2000, Windows 2003, Windows 2008, Windows ME, Windows Vista, Windows 2012.

You can download Portfolio Optimization which is 601.61 KB in size and belongs to the software category Accounting and Billing Software. Portfolio Optimization was released on 2015-04-20 and last updated on our database on 2017-03-08 and is currently at version 5.

Thank you for downloading from SoftPaz! Your download should start any moment now. It would be great if you could rate and share:

Rate this software:

Share in your network:

Portfolio Optimization Description

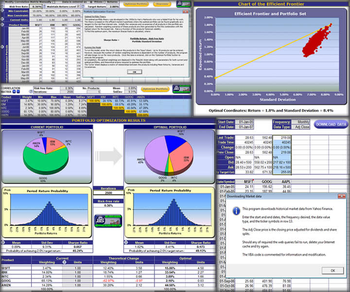

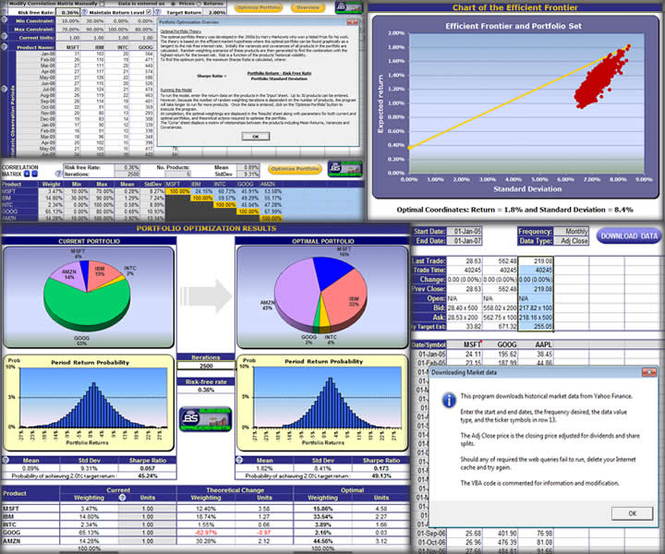

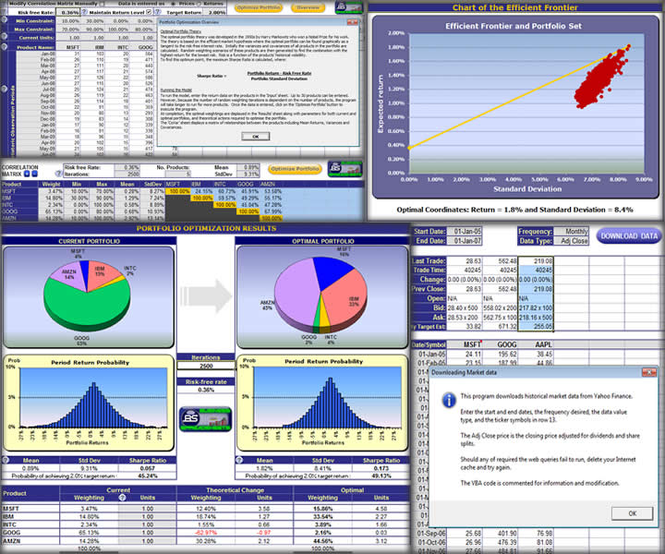

The Portfolio Optimization template identifies the optimal capital weightings for a portfolio of financial investments that gives the desired risk and return profile based on the correlation between individual investments. The design of the portfolio optimization model enables it to be applied to either financial instrument or business stream portfolios with long and short positions. The portfolio optimization template is intuitive and flexible with help icons throughout to assist with input and interpretation of output results. Input of historical data for the analysis is supported by options to specify absolute prices or returns, number of current units held and a tool to download long time periods of financial market data for securities from the internet. Advanced optimization options include setting minimum and maximum constraints for weightings in the optimal portfolio and risk analysis options for overall volatility under the Sharpe ratio, downside risk or semi-deviation under the Sortino ratio and gain/loss under the Omega ratio. Optimization can be set to maintain at least the current level of return and specify a target return for which the probability of attaining is calculated via Monte Carlo simulation. The portfolio optimization results are displayed with weighting charts and return distributions as well as acquisition and liquidation actions required. Technical analysis is provided with back tested total return from signal trading and automatic optimization of technical period constants for each investment or the total portfolio that results in the highest back tested return. Technical analysis indicators with detailed charting and back testing analysis include simple moving average (SMA), rate of change (ROC), moving average convergence/divergence (MACD), relative strength index (RSI) and Bollinger Bands. The template is compatible with Excel 97-2013 for Windows and Excel 2011 or 2004 for Mac as a cross platform portfolio optimization solution.

Where to buy?

Last updated price and discount information 9 years agoupdate now

Windows ME and above

Windows ME and above View Screenshots(3)

View Screenshots(3) Comments

Comments Download

Download

Similar Software

Similar Software Recently Searched

Recently Searched Software Categories

Software Categories Trending Software

Trending Software Like Us

Like Us